In the James Bond film "Goldfinger", the gold-intoxicated villain - the film's namesake - leaves Bond with this thought: "This is gold Mr. Bond. All my life I have been in love with its color, its brilliance, its divine eminence."

Movies like this epitomize the human fascination with this precious metal and the greed that it sometimes inspires. Contrary to what Goldfinger thought, gold may not be the most valuable investment in the world - it may be nothing more than a form of insurance.

Here we look at the major issues facing gold, such as its demand/supply imbalance and its potential to share the same fate as silver. We also revisit the gold standard, and examine what gold really means as an investment.

Gold's Unique Demand/Supply Imbalance

Movies like this epitomize the human fascination with this precious metal and the greed that it sometimes inspires. Contrary to what Goldfinger thought, gold may not be the most valuable investment in the world - it may be nothing more than a form of insurance.

Here we look at the major issues facing gold, such as its demand/supply imbalance and its potential to share the same fate as silver. We also revisit the gold standard, and examine what gold really means as an investment.

Gold's Unique Demand/Supply Imbalance

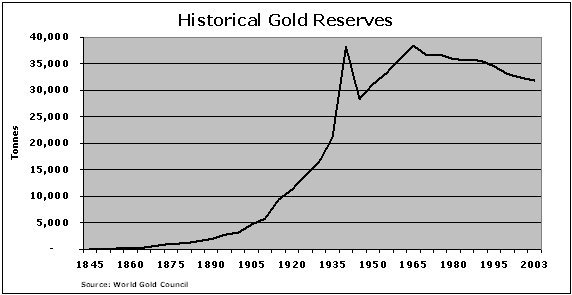

The biggest factor influencing gold's price is the staggering amount of it held by central banks around the world. This is a legacy from the days of the gold standard, which existed in one form or another between 1821 and 1971. During this period, U.S. and European central banks hoarded massive amounts of gold.

According to the World Gold Council, in 2003 this stockpile consisted of 33,000 metric tons, accounting for nearly 25% of all the gold ever mined. In that same year, a total of only 3,200 metric tons of gold was supplied to the marketplace through mining and scrap.

This means that the central banks' stockpile of 33,000 tons could overwhelm the market if it were sold. In other words, there is enough gold in the vaults of central banks to satisfy world demand for 10 years without another ounce being mined! That’s a pretty significant demand/supply imbalance.

Furthermore, without a gold standard, this precious metal has limited strategic use for these central banks. Because gold does not earn any investment interest, some central banks - like that of Canada during 1980-2003 - have already eliminated their gold stock. The potential for gold supply to dwarf its demand poses a hindrance to the metal's potential return well into the future.

Figure 1: Note the gradual decline of the central banks' reserves since the fall of the gold standard. As this decline continues, the price of gold also faces a continual downward stress. Sixty percent of the current gold reserves are held by U.S., Germany, France, Switzerland and Italy. Data provided by the World Gold Council.

Does Silver Foreshadow Gold's Future?

Silver and gold have shared a common history over the past five millennia. Prior to the 20th century, silver was also a monetary standard, but it has long since faded from this monetary scene and from the vaults of central banks around the world. If the current stockpile of gold were to be sold off, the downward pressure on its price could result in it having the same fate as silver.

Perhaps history demonstrates that it is just too difficult for the world to work under a monetary standard based on a commodity because the demand for these metals depends on more than monetary needs.

When these metals were used as monetary standards, the divergence of the market price and mint price for these metals seemed to be in continual flux. (The mint price refers to the price a mint would pay someone to bring gold or silver in to be melted down into coinage.) And continual arbitrage opportunities between market and mint prices created havoc on economies.

The rise and fall of the silver standard - which just happened to be the first victim - perhaps demonstrates how gold's price as a commodity cannot absorb the demand/supply distortions created by its past position as a monetary standard.

The Real Meaning of Gold

So how should an investor really view gold? For the most part, it is a commodity, just like soybeans or oil. So, when making any buy or sell decision, an investor should put future supply and demand issues at the forefront.

At the same time, gold can be seen as a form of insurance against a catastrophic event hitting the global financial markets. However, if that were ever to happen, it's possible that gold would be of use only to those investors who held it physically.

Gold also may be helpful during periods of hyperinflation as it can hold its purchasing power much better than paper money during these periods. However, this is true for most commodities.

Hyperinflation has never occurred in the U.S., but some countries are all too familiar with it. Argentina, for example, saw one of its worst periods of hyperinflation from 1989-90, when inflation reached a staggering 186% in one month alone. In such situations, gold has the capacity to protect the investor from the ill effects of hyperinflation.

Conclusion

Gold means many things to many people. Its history alone has lured some investors. One of gold's most important historical roles has been as a monetary standard, functioning much like today's U.S. dollar. However, with the gold standard no longer in place and industrial demand representing only 10% of its overall demand, gold's luster - as an investment - is not quite as bright.

Gold means many things to many people. Its history alone has lured some investors. One of gold's most important historical roles has been as a monetary standard, functioning much like today's U.S. dollar. However, with the gold standard no longer in place and industrial demand representing only 10% of its overall demand, gold's luster - as an investment - is not quite as bright.

Until the fate of the gold stockpile accumulated by governments is determined, the price of it will have difficulty. Therefore, holding gold as an investment is really a form of insurance against a period of hyperinflation or a catastrophic event hitting our global financial system. However, insurance comes at a price, and is that price worth it?

No comments:

Post a Comment